Money, money, money. The world is run by it, yet for many, personal finance is difficult. In all probability, this is a deliberate circumstance. There is always going to be someone who profits from our inability to manage our money properly. Bad financial choices are so easy to make, good ones are harder because they require a great deal of pro-activity.

Countless movies about guys in suits on Wall Street make finance look like a game. A bit of fun and very exciting. But in fact, it is war. It is extremely hard, and it is not enjoyable unless you are winning.

The world changes constantly, but the rules will not change. They can and should be adapted to fit in with current events such pandemics, inflation and the bull and bear market.

So, here are 7 rules that may help you to stay out of financial trouble:

1. Always have a budget

Have a budget for your monthly outgoings, i.e. food, entertainment and clothes, and stick to it. The goal is to always spend below that budget. If you overspend, deduct it from the next budget period. Be strict about the rules. If you overspend, the next term will become harder and you would need to make it work with less money. Don’t allow margins for error because once you do it once, there is enough justification to do it again, and again, and again.

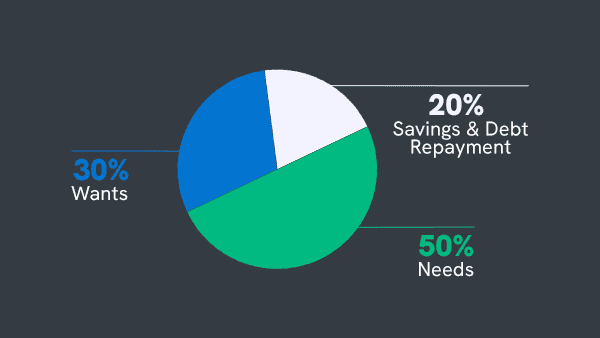

Allocate a budget to your needs, wants and savings. Needs: rent, bills, foods, cost for exercise be it running shoes or the gym membership, necessary clothing. Wants: Any non-essentials, clothes and stuff that you don’t need but want to have for one reason or another. However, make sure that purchases in the wants category are intentional i.e. items that would fulfil a purpose, items that are unique and not just another duplicate of x.

Lastly, add your savings budget to your savings account on the first pay day so you have less in your bank account for the rest of the month.

These days there is an app for everything, including budgeting! Check out our reviews of budgeting apps: Emma, Money Dashboard, Cleo, Snoop.

2. Make monthly saving a habit

Make monthly saving to a habit. How much, is up to you. But there is no harm in trying to challenge yourself. Think bigger in regards to saving and don’t be timid. Put a big chunk into your savings account and see how you get on for an entire month with a lot less than you are accustomed to. Not only will this make you better at saving, but it will also teach you to budget.

3. Avoid buying things on impulse

Buying things on impulse often ends with regrets. If you can, return the items and get a refund! Don’t wait until the cancellation period has passed because of shame or guilt. If you cannot return the item, try to sell it. Selling is better than having to sit on an unwanted item that is not giving you anything!

Always put aside time to think about any purchases and investments. The higher the price, the longer it should take to research whether the purchase or the investment is worthwhile. Do not get swayed into buying something without researching the offer first and getting information from a variety of sources. Don’t get tricked by sales tactics about limited offers, item scarcity, scientific jargon and flattery.

4. Focus on yourself and not others

We want to be loved and respected, and this means that we often purchase things to impress others rather than ourselves. People who are your friends are impressed by you and not the stuff you own. Stop following trends and work on your own personal style. See what whatever you are spending money on is doing for you and how it will enhance your life.

5. Rethink your debts and focus on repaying them quickly

Having debts is a heavy burden. So it is important that the debts that you have are worthwhile. For example, debt because of a property purchase, or a business loan, makes more sense than having maxed out the limit on credits cards with unnecessary purchases. Debt on items that depreciate fast are not great and will end up costing you more if you add the interest. A property or a business can increase in value over time.

Aim for paying off credit cards bills in full and on-time every month. However, if you cannot control your spending and/or repay on time, then perhaps the best options is to cancel your credit cards until you have learned to spend and to budget responsibly. Be truthful to yourself.

There are worst case scenarios to any debt such as debt collectors that hassle you either in person or by post, foreclosure, a bad credit rating that will haunt you far into the future, and having to declare yourself bankrupt. Plus, the toll it takes on your emotional well-being; anxiety and sleepless nights. Debt sticks on you like glue. Whenever you become a bit slack, picture the above scenarios to give yourself that kick you need to get back on track.

When it comes to paying off debt. A sound practice is, to pay off debt with the highest interest first and pay the minimum on the rest. If the interest is low, you can take advantage of the lower rates. But pay it off at some point.

Create a plan about your debt repayment and stay on the path! It will be hard, no question about it. But it is absolutely worth it and you will feel a huge weight lift off your shoulders once you are completely debt free.

6. Increase your income

Make an effort to find ways to increase your income. If you didn’t receive a payrise for a while, ask for one! Have you been eyeing a better position in your company but haven’t had the courage to ask about it? Be brave and express your interest to your boss. If you haven’t got the necessary skills, see if you can get them by taking evening classes. If you are self-employed, maybe you could take on more clients or expand on your offers and products? Or maybe you have a great new business idea?

7. Research how to effectively invest and grow your money

The return on saving accounts is not great these days, but there are other ways to invest such as stocks & shares, bonds and ETF’s. However, do your research before taking any big or small investment decisions. Aim for a diverse portfolio and don’t risk everything on one big investment. Another area to invest in is your own home. Owning your own home will make retirement easier when you don’t have any rent to pay. Don’t forget to think about the future when you make financial decisions. Ask yourself: what will my investment look like in 10, 20, 30 years?

Apps like Plum or Moneybox can help if you have a hard time saving or investing.

Managing personal finance can be time-consuming. However, whatever you learn will stay with you and will be relevant tomorrow. Plus, you can build upon your knowledge as you go, a small step at a time.