There is no guideline, or one fits all rule, on how much money anyone should save per month. However, if you just want to start somewhere, then the 50-30-20 rule is a good place. The rule was first mentioned in a book by Elizabeth Warren, (the Harvard law professor and US senator) and Amelia Warren Tyagi (American Business Woman, management consultant and author), with the title: “All Your Worth: The Ultimate Lifetime Money Plan“.

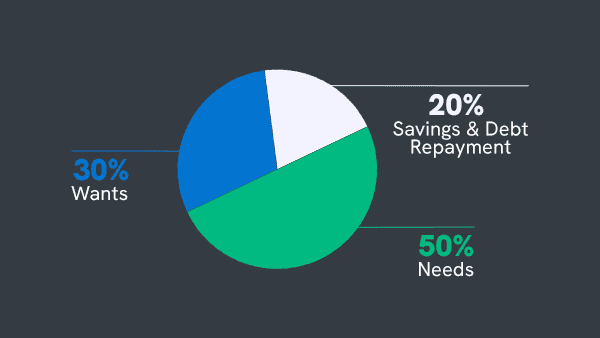

The rule stipulates that 50% of our monthly income should go into essentials i.e. your “needs”. These are housing, bills, insurances, transport and essential food and groceries. 30% should go into non-essentials such as restaurants, non-essential grocery shopping, clothes, entertainment i.e. “the wants”. The remaining 20% should go directly into savings or to pay off debt. This is a good guide to kick off for the absolute beginner.

Following this rule will definitely help you to save money if you stick to it and make a record of your spending. Nowadays, new technology focused ‘challenger’ banks such as Revolut, N26 or Starling Bank have created features within their products that allow you to assign your money into groups within their banking apps. This makes it so much easier to track your spending.

What Are You Saving For?

But, then what next? What are you saving for? What are your plans with this money? Do you have a goal? Remember, current interest rates since the global financial crisis are LOW and inflation is steady at around 2% – 4% per annum. This means your savings are depreciating year on year. At an inflation rate of 4%, your 10,000 in savings this year will only be worth 9,600 in the next year. That is a problem. Saving should not only be about savings, i.e. accumulating money without a goal in mind, but should build a sustainable foundation for you.

What do you want to save money for? For a nest-egg? And how much should you keep in your nest-egg? Having liquidity, i.e. cash on hand, is always good for added security, i.e. unforeseen events and expenses.

Plus, you will not be forced to sell some of your assets at a loss while the market is not in your favour.

However, having liquidity is not only for serving you in bad times, it could be advantageous towards unforeseen opportunities as well.

Though, having large chunks of cash sitting in your savings account doing literally nothing for you might be bad money-management. The sum of how much liquidity one should keep should be set on an individual basis, depending on your life circumstances. For example: job stability and family planning, or a huge promotion.

Investment Options

There are various options what you could do with your money, investing in land, property, companies, cryptocurrency, commodities, stocks and bonds etc. This is not advice on how to invest your money. Rather, it is a gentle steering towards the thinking about the various possibilities on what to do with your money. There is no one size fits all. But having a plan or many plans, and spending actual time thinking about your goals, is still better than saving for the sake of just saving.

If you are already in retirement and have a chunk of money sitting in your account, you are likely risk-averse because you simply might not have the time to recoup any loses, so a loss of an inflationary 4% won’t be such a big deal. That is okay too, because you have made an informed, calculated decision about it.

However, when you are still young and at your prime of earning potential, it might be a completely different story. You still have a lot of time to put money away. Be it for early retirement, to buy property or to travel. All of these are fine as long as you have a goal. Because pursuing any of these would require a different approach on how to save. If you are saving for retirement, you could, for example, look at long-term investment opportunities such as stocks and shares, that offer both growth potential and regular dividend payments. But be aware that trading with any stocks and shares does come with the risk of losing it all. And anyone who has invested into stocks has seen losses. It requires patience, research and diversification across various industries.

So, saving should always come with a goal in mind and effective money-management so that you get good returns on your money. The good thing is there is plenty of information around. Do your research and get involved!

Rules Are Made To Be Improved

Once you know what you want to save money for, the 50-30-20 rule can change. If you want to buy property, then perhaps you want to save additional money by moving somewhere cheaper. And suddenly the 50-30-20 rule can become a 40-30-30 rule. For example, if you live in a big city where rent is astronomical, but would like to buy something. You could move into a location outside of the city, where you could afford to buy, and where it is cheaper to rent. By renting first you can get a feel for the area before committing to a life changing purchase.

If you want to save more because you want to get faster to a mortgage down-payment, change the 50-30-20 rule to 40-20-40. Live lean for a year and spend less on entertainment, clothes and restaurants.

In conclusion – the 50-30-20 rule is a great starting point if you want an answer on how much one should save per month. The real work begins when finding out what the money is supposed to be used for and how to manage it effectively so that it will grow and become an asset over time.